Originally published on X: View source thread

Crypto does not need another essay explaining that incentives are mercenary. Everyone knows that already. The more interesting question is harsher: what do we make of the cases that are supposed to count as successes?

Unichain is one of the best test cases because this was not a weak team flailing around with farm tokens. This was @Uniswap, working with @Gauntlet, with real brand, real distribution, real liquidity gravity, and real money behind the campaign.

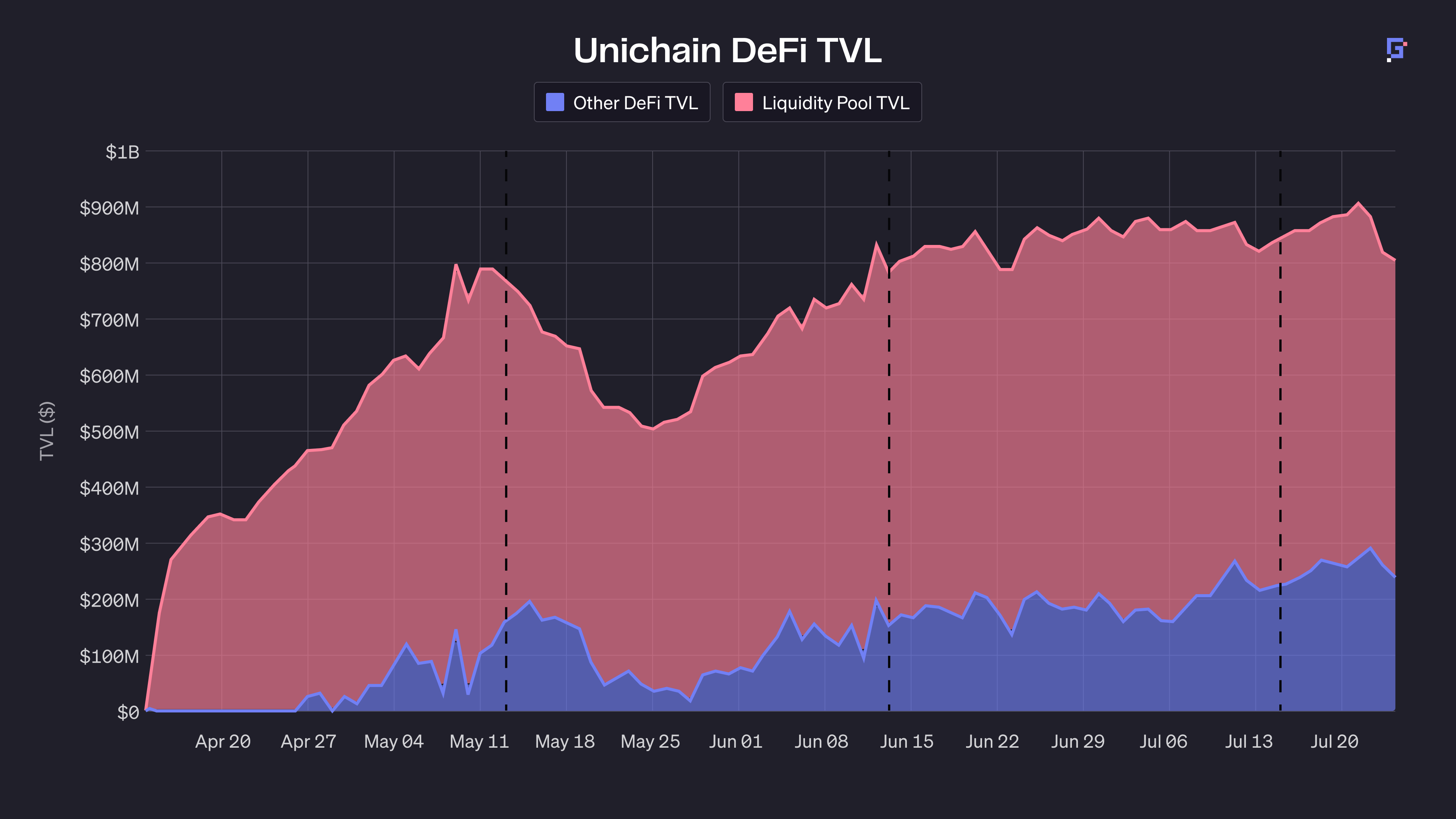

Gauntlet's own numbers made the program look like a winner. Its 3-month retro says the Unichain campaign launched on April 14, 2025 with $21.8 million of incentives, or 3.5 million UNI, under a broader $45 million governance-approved budget across Unichain and Uniswap v4. The stated goal was to push Unichain to $22.5 billion in volume. Gauntlet says the campaign reached $32.8 billion in cumulative volume, pushed chain-level TVS from roughly $4 million–$8 million before launch to a peak of $1.4 billion, and hit all KPI targets by June 21, three weeks early, while using only 3.3 million UNI, leaving a 198,000 UNI surplus.

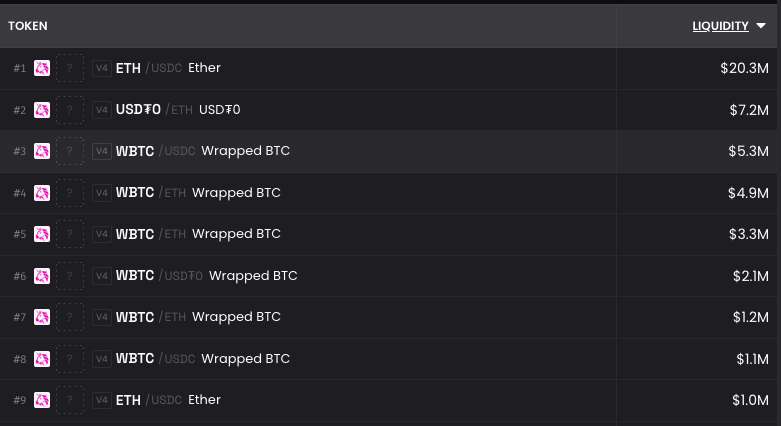

That report did not just claim rented activity. It claimed transition. Gauntlet said blue-chip pools such as ETH/USDT0, USDC/ETH, and WBTC0/USDT0 had moved to organic fee-driven revenue, with base yields exceeding incentive yields and accounting for more than half of LP revenue. It called ETH/USDT0, USDC/ETH, WBTC0/USDT0, and WBTC0/USDC pools with “positive sustainability signals,” and went as far as saying they had made a “successful transition to self-sustaining liquidity ecosystems.” Its hero case was WBTC0/USDT0: $1.7 billion cumulative volume, $36 million TVL at campaign end, 60% market share versus comparable pools on other chains, and 75% of LP returns from organic trading fees.

The report explicitly says fixed incentive programs usually suffer when rewards expire. It also says the campaign had not yet achieved the full virtuous cycle where volume-driven base yields themselves attract more TVL organically. And it says TVL growth had already begun to stabilize, with diminishing returns from additional spend. That is the whole problem in miniature: the market looked healthy, but even Gauntlet was admitting it had not fully crossed the bridge from subsidized success to organic permanence.

Now look at where Unichain sits today. DefiLlama currently shows about $48.45 million DeFi TVL, $174.24 million stablecoin market cap, $145.12 million bridged TVL, and $21.98 million in 24-hour DEX volume.

The pool-level picture is what makes the postmortem interesting. Some of Gauntlet's “winner” pools are still alive. USDC/ETH still shows roughly $20.3 million liquidity and $5.8 million 24-hour volume. ETH/USDT0 still has about $7.2 million liquidity and $665,000 daily volume. WBTC/USDC sits around $5.3 million liquidity and $444,000 daily volume.

The hero pool Gauntlet celebrated most aggressively, WBTC0/USDT0, is now around $2.1 million liquidity and $121,000 24-hour volume. Against Gauntlet's own $36 million campaign-end TVL figure, that is roughly a 94% drop in liquidity. The strongest campaign-period proof point still turned out to be much more contingent than the victory lap suggested.

Incentives do not only fail by failing. They often fail by succeeding incompletely. If they do not push the broader system into a truly self-sustaining equilibrium, then the peak becomes a very expensive temporary state. Unichain is the clean example of that dynamic: a campaign strong enough to post blockbuster numbers, but not strong enough to make those numbers durable in the way the headline implied.

Why This Matters Beyond Unichain

A huge amount of capital in crypto is still pulled in by some form of yield, points, rebates, staking return, or incentive layer. The costume changes; the primitive does not. The problem is that those flows are, by definition, hard to sustain forever. If the reason capital came was a temporary economic sweetener, then the system eventually has to answer a brutal question: what remains when the sweetener normalizes?

That is why crypto needs a different tool. The standard crypto answer to fragile participation is still “add more upside.” But the real reason capital hesitates is usually the downside: fear of being the one left holding the bag when the bootstrap ends. That is why downside protection is a more coherent primitive than raw incentives. Rather than paying people to show up and hoping they stay, it changes the payoff profile of participating in the first place.

Exchequer is one of the few teams explicitly building in that direction: its material frames Protected Preferred tokens as combining full upside exposure with configurable downside protection, while creating protocol-owned liquidity as an alternative to emissions-heavy liquidity programs.

So the postmortem on Unichain is uncomfortable: if Uniswap, with Gauntlet, tens of millions of dollars, and one of the strongest brands in DeFi can produce this kind of outcome, then smaller projects should stop pretending incentives are a reliable path to durable growth.